Imagine an appraisal comes in at $860,000 on a $900,000 California escrow, and the immediate reaction is usually a mixture of panic and blame. The seller feels insulted, the buyer feels they are overpaying, and both agents often get trapped in an emotional spiral.

In my 20+ years coaching California agents and keeping tons of escrows together, I’ve learned that a low appraisal is not an automatic emergency.

It is a process problem.

When the value doesn't come in at the contract price, you don't need a miracle; you need an operating system. This guide provides the tactical decision tree and scripts necessary to bridge the gap and maintain a broad set of Real Estate Agent Skills.

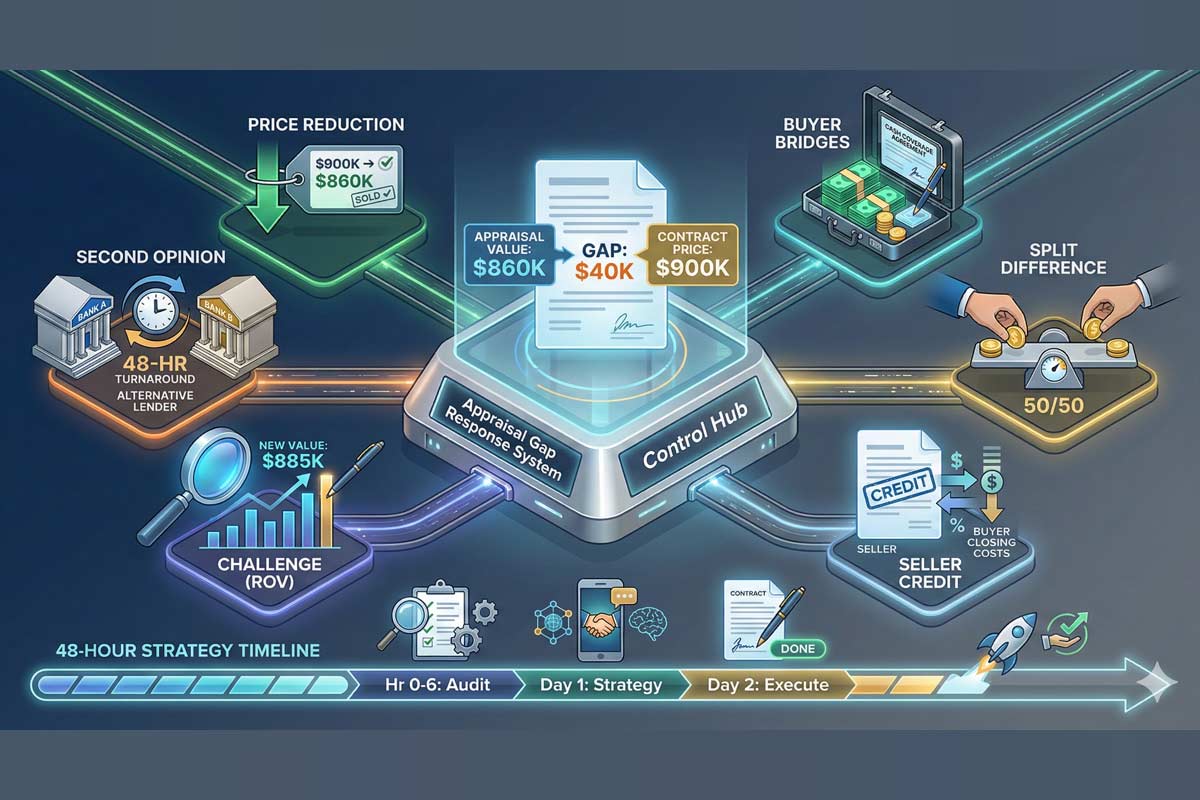

Most agents freeze because they don’t understand the lender's logic. In any financed transaction, the loan amount is based on the lower of the purchase price or the appraised value.

The Example:

If your buyer is putting 20% down ($180,000), they expected a loan of $720,000. Because the appraisal hit $860,000, the bank will now only lend 20% of that value ($688,000). That $32,000 difference in loan proceeds—plus the original down payment—is what the buyer must now "bridge" with cash or negotiation. Knowing how to explain contract terms to clients clearly is the only way to keep them calm when these numbers shift.

The seller drops the price to $860,000.

The buyer brings the $40,000 difference in cash.

Seller drops to $880,000; Buyer brings extra cash but the seller still takes a haircut.

The seller gives a credit to the buyer for closing costs, which frees up the buyer’s cash to cover the $40,000 gap.

Requesting a Reconsideration of Value (ROV) by providing 3 new comps.

Moving the file to a new lender to get a fresh appraisal.

"The appraisal came in at $860,000. This is a normal lender constraint we see in appreciating markets. To keep this on track for our closing, we need to decide if we want to ask the buyer to bring the $40,000 difference, adjust our price, or find a middle ground. Given our backup offers, I suggest we hold firm on price but offer a small credit to help their liquidity."

"The report is light by $40,000. My seller knows the value is there. If we were to go back on the market today, we'd have five new offers by Monday. Let’s look at the cash-to-close. If my seller meets you $15k of the way, can your buyer bridge the rest to keep their rate lock in place?"

"I understand the frustration. Practically speaking, however, any new buyer with a loan will likely face this same appraisal value. If we cancel now, we lose 21 days of market time and still have to deal with this $860,000 ceiling with the next lender.""

One of the most frequent deal-killing mistakes occurs in the documentation phase.

An appraisal gap is a test of your ability to manage expectations and math simultaneously. By removing the emotion and applying a clinical operating system, you protect your client’s interests and your commission.

Ready to stop "winging it" and start mastering the full Real Estate Agent Skills California stack?

What is an appraisal gap?

It is the difference between the contract price and the appraised value.

Can the seller dispute the appraisal directly?

No. In most cases, the dispute (ROV) must be initiated by the buyer through their lender, though the listing agent provides the data.

How long does an ROV take?

Typically 2 to 5 business days, depending on the lender’s internal review board.

Do seller credits solve a low appraisal?

Only if the buyer’s main hurdle is cash. It does not change the loan-to-value (LTV) limits set by the bank.

Should I release contingencies before the appraisal?

Generally, no. Unless your buyer has explicitly agreed to an "appraisal gap coverage" or waived the contingency to win a bidding war, you should wait for the report.

Disclaimer: This article is for educational purposes only and does not constitute legal or lending advice. Always consult with your broker and the buyer’s mortgage professional regarding specific transaction details.

Founder, Adhi Schools

Kartik Subramaniam is the Founder and CEO of ADHI Real Estate Schools, a leader in real estate education throughout California. Holding a degree from Cal Poly University, Subramaniam brings a wealth of experience in real estate sales, property management, and investment transactions. He is the author of nine books on real estate and countless real estate articles. With a track record of successfully completing hundreds of real estate transactions, he has equipped countless professionals to thrive in the industry.

"Hey guys,

I took the exam today and passed!!!!

It only took me one try which was one of my goals. I took the online

classes and follow your suggestions so I took the crash course,

used the crash course app a lot, took 7 mock tests and went

confident to present the exam. Thank you for the great job you are

doing, you guys are awesome!!!! May God continue to bless you!"

Willie V.