California Title Insurance: Protect Against Hidden Encumbrances

Have you ever heard a story about someone purchasing a home only to discover later that someone else claimed partial ownership or that Read more...

California Title Insurance: Protect Against Hidden Encumbrances

Have you ever heard a story about someone purchasing a home only to discover later that someone else claimed partial ownership or that an unpaid lien remained attached to the property? Issues like these can turn a dream home into a financial nightmare.

A property can have various ‘burdens’ on its title and while California law requires sellers to disclose known encumbrances, unforeseen issues can still surface. That’s where title insurance comes in. This article explains what title insurance is, what it covers, how it works, and why it’s so crucial for homebuyers in California.

What is Title Insurance?

Title insurance is a specialized insurance policy designed to protect your ownership rights and financial investment in real estate. Unlike homeowners’ insurance, which covers future events like fire or theft, title insurance safeguards you against past events that might affect the validity of your property’s title.There are two main types of title insurance policies:

Owner’s Policy: This policy protects the buyer’s interest in the property. It covers you up to the purchase price, shielding you from potential legal costs or financial losses if any undiscovered issues arise.

Lender’s Policy: Almost always required by lenders, this policy protects the mortgage company’s interest (usually up to the loan amount). If you finance your home with a mortgage, your lender will insist on a lender’s policy to ensure its investment is protected.

What Does Title Insurance Cover?

Title insurance shields you from problems that could emerge from previous owners or mistakes in the public record. Below are five common scenarios (out of many) that title insurance might cover:

Undisclosed Encumbrances: Sometimes, encumbrances such as easements or liens don’t appear in the initial public record search. For example, an easement that wasn’t properly recorded could give third-party rights to your property. Additionally, unpaid property taxes, mechanic’s liens (filed by contractors or builders for unpaid work), judgment liens, or even unrecorded mortgages may exist without your knowledge.

Errors in Public Records: Even minor clerical errors in deeds or misindexed documents can create significant complications. Mistakes like a misspelled name or wrong property description could lead to ownership disputes.

Fraud and Forgery: Unfortunately, identity theft and document forgery are realities in real estate. A past owner’s signature might have been forged on a deed or other legal document. Title insurance covers financial losses you could incur if you must defend your ownership against fraudulent claims.

Claims from Heirs: In some cases, a property might have been passed down through inheritance, and an undisclosed heir could appear, claiming rightful ownership or interest in the property. Title insurance protects you from these unexpected claims.

Boundary Disputes: Encroachments, as we learned, are a type of encumbrance. They arise when a fence, shed, or other structure crosses a boundary line. If a past survey was inaccurate or if a structure was built in the wrong place, you could face legal or financial consequences.

Real-World Example:

Imagine buying a home, moving in, and then receiving a notice stating that a builder had never been paid for renovations done by the prior owner. This builder filed a mechanic’s lien, which went unnoticed. Title insurance would pay off or resolve this lien, sparing you a significant financial burden.

The Title Search and Commitment

Before issuing a title insurance policy, the title company thoroughly examines county records, court filings, and other public documents to uncover any problems or “clouds” on the title. This extensive research helps identify mortgages, liens, easements, or other encumbrances that might affect ownership.

Once the search is complete, the title company issues a “title commitment” or “preliminary report.” This document details all the findings and lists any “exceptions” that the policy will not cover. Standard exceptions might include existing easements or restrictions on the property. It’s crucial for buyers (and their real estate agents or attorneys) to carefully review the title commitment before finalizing the purchase. If any red flags appear, you can address them or negotiate with the seller before closing.

How Much Does Title Insurance Cost?

Title insurance is typically a one-time premium paid at the real estate transaction's closing. In California, the cost varies based on the home’s purchase price and the county. It’s customary in many parts of California for the seller to pay for the owner’s policy, but this is negotiable.

Why is Title Insurance Important?

Financial Protection: Title insurance can save you from hefty legal fees or financial losses if a hidden title defect surfaces.

Peace of Mind: Knowing your ownership is shielded from past claims helps you focus on enjoying your new home.

Facilitates Future Transactions: A clear and insured title makes it easier to sell or refinance. Prospective buyers or lenders feel more comfortable knowing your property’s title is clean.

Legal Defense: Many title insurance policies cover the costs of defending against lawsuits challenging your ownership. In short, title insurance protects your wallet and your peace of mind.

Title insurance is crucial in the California home-buying process, ensuring that hidden encumbrances or past errors won’t jeopardize your investment. Discuss coverage details with your real estate agent, lender, or attorney for the best protection—putting into practice what you learned in real estate school.

Love,

Kartik

|

Entering the real estate world and finishing your real estate classes is exciting, but landing those first few listings can feel daunting. I know you're putting in the effort, but even minor missteps can Read more...

Entering the real estate world and finishing your real estate classes is exciting, but landing those first few listings can feel daunting. I know you're putting in the effort, but even minor missteps can cost you valuable clients. Don't worry, I’m here to help! This article explores 12 common mistak

|

Effective January 1, 2025, Assembly Bill 2622 (AB 2622) significantly changes California's contractor licensing requirements. This update directly affects real estate agents, brokers, investors, Read more...

Effective January 1, 2025, Assembly Bill 2622 (AB 2622) significantly changes California's contractor licensing requirements. This update directly affects real estate agents, brokers, investors, and homeowners who hire individuals for home improvement or construction projects. Below, I will explore the key elements of AB 2622, why it matters even if you are just starting real estate school, and how real estate professionals can use this knowledge to serve their clients better and protect their interests.

Key Changes Introduced by AB 2622

A. Increased Exemption Limit

Under prior law, unlicensed individuals could perform construction work if the total cost of labor, materials, and other project expenses did not exceed $500. Under AB 2622, this threshold is raised to $1,000, effectively allowing unlicensed persons to handle more minor jobs without violating California's Contractors State License Law.

B. Building Permit Requirement

The new exemption applies only if no building permit is required. If the scope of work triggers a building permit—for example, electrical rewiring, plumbing changes, or structural modifications—an unlicensed individual cannot legally take the job. In such cases, a licensed contractor is mandatory.

C. Restriction on Employing Others

A critical addition is that unlicensed individuals under this exemption cannot employ any other person to perform or assist with the work. When another individual is brought on board—whether paid or unpaid—the exemption no longer applies, and a contractor's license is required.

Impact on the Real Estate Industry

A. Real Estate Agents and Brokers

1. Avoiding Liability

Proper Disclosures: When representing clients, listing agents and sellers should confirm whether any recent renovations fall under this new $1,000 limit and whether permits were required but not obtained. Disclosing unpermitted or incorrectly permitted work could expose liability issues.

Compliance Check: By understanding AB 2622, agents can spot red flags—like multiple small jobs potentially split to avoid licensing requirements—thereby safeguarding clients from legal disputes.

2. Negotiation Leverage

Price Adjustments: Knowledge of whether work was performed by a licensed contractor or an unlicensed individual can significantly affect property valuations. Unpermitted work or questionable quality might justify a lower offer or prompt a repair request. Conversely, adequately documented upgrades can bolster a seller’s asking price.

Confidence in Transactions: A firm grasp of these regulations allows agents to negotiate more effectively. Agents identifying compliance issues can use that information to protect their clients' interests and potentially secure better terms.

3. Building Trust and Credibility

Demonstrating Expertise: Clients value real estate professionals who can expertly navigate the complex web of state regulations. By explaining AB 2622 and its implications, agents position themselves as a trusted advisor, which can lead to stronger referrals and repeat business.

Professional Growth: Continued real estate education on legislative updates helps agents maintain a competitive edge and enhances their reputation in a crowded marketplace.

B. Real Estate Investors

1. Permitting Nuances

Local Codes: Depending on local building codes, even smaller jobs—like adding electrical outlets or replacing certain plumbing fixtures—might trigger permit requirements. Investors should do due diligence before starting any project.

Avoiding Costly Mistakes: Failing to secure permits when required can lead to fines, forced rework, and delayed timelines that eat into profit margins.

2. Cost Savings vs. Quality Concerns

Safety Issues: Hiring an unlicensed individual can save money, but the risk of subpar workmanship is real. Poor electrical or plumbing work can create health or safety hazards, hurting the property's long-term value.

Hidden Problems: Unlicensed work may introduce latent defects, issues that surface after the project is complete and potentially cause expensive repairs.

Insurance and Financing: Coverage or financing can be jeopardized if an insurer or lender discovers that work was done improperly or without the proper permits. Some insurance policies may exclude damages stemming from unlicensed or unpermitted work.

3. Long-Term Marketability

Resale Considerations: When an investor plans to flip or rent out a property, prospective buyers and tenants often ask about the quality of renovations.

Balancing Act: Using an unlicensed individual may make sense for tiny, simple tasks under $1,000. However, hiring a licensed contractor is often safer for anything potentially requiring a permit or multiple workers and may improve the property's overall appeal.

C. Homeowners

1. Due Diligence

Insurance Review: Before hiring an unlicensed individual for small projects, homeowners should check whether their insurance covers injuries or damages from unlicensed work. Some policies have exclusions.

Written Contracts: Even for minor tasks, having a written agreement that outlines the scope of work, payment terms, and timelines can prevent disputes.

Confirm Permits: Always verify if a building permit is required. If so, the homeowner must hire a licensed contractor regardless of the project's cost.

2. Risks and Benefits

Potential Cost Savings: The increased $1,000 threshold can make minor repairs or aesthetic updates more affordable for homeowners.

Liability and Quality: Hiring an unlicensed individual may leave the homeowner limited legal recourse if the job goes wrong. Always weigh immediate cost savings against the potential for future headaches.

3. Staying Compliant

Avoiding Fines: Projects without the required permit can lead to penalties and complications during a future sale.

Protecting Property Value: Quality, properly documented work generally enhances a home's value, while unpermitted or shoddy work could detract from it.

Advertising Changes Under AB 2622

Unlicensed individuals may now legally advertise for jobs under $1,000 provided:

No Permit Required: The work doesn't trigger any building permit requirements.

Clear Disclosures: The advertisement explicitly states: "I am not a licensed contractor."

Solo Work: Unlicensed people cannot employ anyone else to assist with the job.

Misrepresenting licensure status or splitting a more extensive project into multiple smaller ones (each under $1,000) to evade these rules is illegal and can lead to penalties.

or lead to financial losses.

Your Next Steps

1. Read the Full Text of AB 2622

For the exact language of the law, visit the California Legislative Information website and review Business and Professions Code Sections 7027.2 and 7048.

2. Consult the Contractors State License Board (CSLB)

Check a contractor's license status or learn more about licensing requirements by visiting the CSLB website.

3. Consider Continuing Education

Whether you're an agent seeking to differentiate yourself, an investor optimizing your strategies, or a homeowner ensuring compliance, staying educated on these laws is crucial. Find reputable real estate courses or legal resources that delve into contractor licensing, property disclosures, and best practices.

4. Perform Due Diligence

Confirm if a building permit is required. Always get references, a written scope of work, and proof of insurance—even if the work seems small.

AB 2622 introduces critical updates to California's contractor licensing laws by raising the exemption threshold to $1,000, clarifying the need for building permits, and restricting unlicensed individuals from hiring help. These changes affect real estate agents, brokers, investors, and homeowners, influencing how renovations are approached, disclosed, and negotiated.

Understanding these regulations can provide:

Liability Protection for real estate professionals who accurately disclose property improvements.

Investment Security for those fixing and flipping properties or building their rental portfolios.

Peace of Mind for homeowners making small-scale improvements while avoiding legal pitfalls.

Staying informed is half the battle, and resources are available to help you succeed. By taking advantage of educational programs and consistently monitoring regulatory updates, you'll be well-prepared to navigate California's evolving real estate landscape.

With AB 2622 having taken effect on January 1, 2025, now is the time to proactively adapt, ensuring you and your clients remain compliant and well-informed in California real estate.

Love,

Kartik

|

Want to be a top-performing real estate agent? Then you need to go

beyond the basics of real estate license school and understand the

practical roles of home inspectors, appraisers, and title officers.

Mastering Read more...

Want to be a top-performing real estate agent? Then you need to go

beyond the basics of real estate license school and understand the

practical roles of home inspectors, appraisers, and title officers.

Mastering these collaborations is the key to smoother transactions,

happier clients, and a str

|

Studying for the California Real Estate Exam can feel overwhelming.

According to data from the California Department of Real Estate (DRE), the pass rate often hovers between 40-55% for first-time test Read more...

Studying for the California Real Estate Exam can feel overwhelming.

According to data from the California Department of Real Estate (DRE), the pass rate often hovers between 40-55% for first-time test takers—so

every point matters! One thing that frequently trips students up is how

questions are

|

Buying a home involves many moving parts—financing, property searches, negotiations, inspections, and closing steps. For clients, it can be an exciting yet sometimes confusing experience. As a real estate Read more...

Buying a home involves many moving parts—financing, property searches, negotiations, inspections, and closing steps. For clients, it can be an exciting yet sometimes confusing experience. As a real estate professional, a well-planned home-buying checklist is one of the most effective tools available to guide buyers smoothly through the process.

A thoughtful checklist keeps everyone on the same page, clarifies responsibilities, and ensures no step is overlooked. You demonstrate your organizational skills, show a genuine commitment to client success, and create a more streamlined, stress-free transaction.

In this guide, I will break down each phase of the home-buying journey and explain how to incorporate a checklist that supports your clients and elevates your practice. By the end, you’ll know how to build and share a custom checklist that distinguishes you as a forward-thinking, service-driven agent.

Why Checklists Are Essential

A professionally crafted home buying checklist achieves several goals at once. It:

Encourages Transparency: Clients can see each stage of the process, reducing uncertainty and misunderstandings.

Instills Confidence: By mapping out every step, you help buyers feel secure in the path ahead.

Promotes Efficiency: Having a reference guide at your fingertips helps you manage tasks and timelines more effectively.

Sets a Higher Standard: Providing a checklist is a simple way to show that you’re not just knowledgeable—you’re also prepared, proactive, and ready to go the extra mile.

Stage 1: Pre-Approval and Financing

Why This Matters:

Securing financing early gives buyers a clear price range and strengthens their bargaining power when making an offer.

How Agents Can Help:

Suggest Reputable Lenders: Offer clients a short list of trusted lenders, so they don’t waste time searching.

Explain Key Concepts: Clarify differences between pre-qualification and pre-approval. Help clients gather the right documents so they can move forward quickly.

Key Checklist Items:

Get pre-approved for a mortgage

Collect and organize financial documents (W-2s, tax returns, bank statements)

Compare loan products and interest rates

Stage 2: Defining Needs and Wants

Why This Matters:

A clear picture of must-haves and nice-to-haves ensures clients focus on properties that genuinely fit their goals.

How Agents Can Help:

Facilitating Priorities: Have clients separate essential features (like a certain school district or a minimum number of bedrooms) from extras (such as a finished basement).

Aligning Expectations with Reality: If a client wants a large yard but has a limited budget, show them examples of comparable listings that might mean considering a slightly smaller lot or a home a bit farther from the city center.

Key Checklist Items:

Create “Must-Have” and “Nice-to-Have” lists

Set a realistic budget after reviewing desired features

Discuss market conditions and common trade-offs

Stage 3: Finding a Real Estate Agent

Why This Matters:

The right agent provides guidance, insights, and local knowledge that clients can’t always get from online searches.

How Agents Can Help (Positioning Yourself):

Highlight Expertise: Show clients that you use a well-structured checklist to keep everything organized and on track.

Establish Credibility: Present testimonials, success stories, and your track record so they know they’re in capable hands.

Key Checklist Items:

Research agents’ experience, market knowledge, and communication style

Seek referrals and read reviews

Interview a few agents to find the right fit

Stage 4: House Hunting and Viewings

Why This Matters:

With multiple homes to consider, clients can quickly lose track of which property offered what benefits.

How Agents Can Help:

Streamlined Showings: Prepare a viewing schedule and a simple rating sheet (e.g., House Hunting Checklist) for each property.

Encourage Note-Taking: Advise clients to take photos and jot down pros and cons. After tours, help them sort through details to find the best matches.

Specific Example:

If clients are torn between a downtown condo and a suburban home, use a rating system to compare key factors: commute, amenities, school districts, and property condition.

Key Checklist Items:

Arrange showings with clear property details

Use a House Hunting Checklist to compare homes

Take notes and review findings to narrow down options

Stage 5: Making an Offer

Why This Matters:

When it’s time to make an offer, a methodical approach ensures buyers put their best foot forward and protect their interests.

How Agents Can Help:

Market-Based Advice: Provide recent comparable sales data to determine a fair offer price.

Contingency Guidance: Suggest sensible contingencies (like an inspection or appraisal) that safeguard the buyer’s position.

Prompt Action: Have all documents ready so you can submit the offer quickly, especially if time is critical in a competitive market.

Key Checklist Items:

Review comparable sales and price trends

Determine offer details and contingencies

Submit a well-prepared offer promptly

Stage 6: Inspections and Appraisal

Why This Matters:

No one wants unpleasant surprises. Inspections and appraisals confirm the property’s condition and value.

How Agents Can Help:

Recommending Professionals: Provide a shortlist of quality inspectors. Explain what clients can expect from the inspection process.

Navigating Results: If the inspection reveals issues, discuss options—such as requesting repairs or a price adjustment.

Handling Low Appraisals: Offer strategies for renegotiation if the appraisal comes in lower than expected.

Key Checklist Items:

Schedule and attend the home inspection

Review the inspection report and negotiate if needed

Confirm the appraisal and address any discrepancies

Stage 7: Closing the Deal

Why This Matters:

The final step involves paperwork, legal details, and timing. It’s essential to stay organized to prevent last-minute stress.

How Agents Can Help:

Track Key Dates: Keep clients informed of all deadlines and requirements leading up to closing day.

Clarify Closing Costs: Break down what to expect in terms of fees, taxes, and insurance so clients aren’t caught off guard.

Final Checks: Remind buyers to complete a final walkthrough to ensure the home is in the agreed-upon condition.

Key Checklist Items:

Obtain final mortgage approval

Review the Closing Disclosure

Conduct a final walkthrough before signing

Sign all documents and receive the keys

Stage 8: Moving In

Why This Matters:

Support doesn’t end at closing. Helping clients get settled cements your role as a caring, full-service advisor.

How Agents Can Help:

Moving Tips: Provide a checklist for transferring utilities, updating addresses, and finding reputable movers.

Post-Closing Follow-Up: Check in after they move to show genuine care and maintain a positive relationship. This attention often leads to referrals and repeat business.

Key Checklist Items:

Arrange for movers and label boxes

Transfer utilities and update address records

Unpack and enjoy the new home

Sample Home Buying Checklist (For Agents to Customize)

Consider offering a detailed version as a branded PDF that you can email to clients or make available on your website. Include your logo, contact info, and any special tips to add value.

Stage

Key Tasks

Pre-Approval

Get pre-approved, gather financial docs, compare loan rates

Needs & Wants

List must-haves vs. nice-to-haves, review budget & market

Find an Agent

Research experience, read reviews, interview potential agents

House Hunting

Schedule showings, use a rating sheet, compare pros/cons

Making an Offer

Check comps, set offer terms, add contingencies

Inspections/Appraisal

Schedule inspections, review report, negotiate repairs, confirm appraisal

Closing

Finalize loan, review disclosures, do a final walkthrough

Moving In

Arrange movers, set up utilities, update addresses, unpack

Educational Value for Your Career

Integrating a home-buying checklist into your approach gives you more than just an organizational tool. You’re refining how you serve clients, setting yourself apart as a resource providing clarity rather than confusion. Your efficiency and preparedness showcase your professionalism, making you the kind of agent clients eagerly recommend to friends and family.

As you continue to use and adapt your checklist, you’ll fine-tune your process, improve your time management, and stay one step ahead of potential challenges. This systematic method strengthens your reputation, enhances client satisfaction, and fosters long-term success in your real estate career.

Your Next Step: Create Your Own Branded Checklist

Now that you’ve seen the advantages of a structured, transparent roadmap, it’s time to develop your own. Customize it to reflect your style, local knowledge, and the unique needs of your market. Provide it to clients upfront so they know what to expect and recognize that they work with a dedicated, detail-oriented professional.

By implementing this simple yet impactful tool, you’ll enhance the client experience and solidify your reputation as a trusted, organized expert. Over time, this approach will help you stand out, earn more referrals, and ensure your clients reach their home-buying goals confidently and efficiently.

A home-buying checklist can transform your clients' experiences and your own workflow. It clarifies a complex process, showcases your professionalism, and empowers buyers to understand each step. By making it a central part of your service, you set a strong foundation for lasting client relationships, repeat business, and a thriving real estate career.

Love,

Kartik

|

Generating real estate leads can feel overwhelming, but did you know that you can generate business without solely relying on online ads. By focusing on real estate networking and building your referral Read more...

Generating real estate leads can feel overwhelming, but did you know that you can generate business without solely relying on online ads. By focusing on real estate networking and building your referral program, you can strengthen your real estate business through genuine connections. In-person meetings, community involvement, and strong relationships with centers of influence are crucial in generating real estate leads and creating a steady flow of clients. These personal connections will help you become a local expert on home values and market trends.

Mastering Real Estate Networking at Events

Attending local industry events, community fairs, and neighborhood gatherings is a proven way to attract real estate clients. The effectiveness of face-to-face interactions at these events allows you to build trust, stand out among other real estate agents, and ultimately generate leads that can turn into profitable referrals.

Prepare a Strong Elevator Pitch

Keep It Short: In 30 seconds, explain who you are, what you do, and who you help.

Highlight Your Specialty: If you’re a buyer’s agent specializing in first-time homebuyers or a seller’s agent focusing on property listings, mention it.

Example: “Hi, I’m Jane Smith, a local real estate agent helping first-time homebuyers navigate the market and find their dream homes.”

Make Meaningful Connections

Ask Questions: Inquire about their needs, such as buying a first home or exploring market trends in the area.

Listen Carefully: Show genuine interest, and offer a helpful tip about local home values or popular neighborhoods.

Quality Over Quantity: Focus on a few strong contacts rather than simply handing out dozens of business cards.

Follow Up Promptly

Send a Friendly Note: A short email or social media message referencing what you discussed.

Offer Value: Share a helpful article on local property listings or a guide to understanding market trends.

Build Trust Over Time: Consistent follow-ups turn a casual chat into a reliable referral source.

Building Relationships With Centers of Influence (COIs)

Centers of influence—like mortgage brokers, attorneys, and financial advisors—can guide their clients to you, helping you generate real estate leads with less effort. By forming strong connections with these trusted professionals, you gain access to their client base and raise your profile as a go-to real estate agent.

Tips for Working With COIs

Offer Value First: Refer a client needing a home loan to a dependable mortgage broker.

Frequent Contact: Set up monthly coffee meetings or send regular updates on home values, property listings, and local market trends.

Provide Useful Resources: Share guides on buying or selling homes, and keep them updated on zoning changes or community developments that influence real estate marketing.

Over time, your centers of influence will recognize you as a trustworthy partner who can handle their clients’ real estate needs.

Building a Strong Real Estate Referral Network

Cultivating a strong referral network is essential for sustained growth in the real estate business. It's about building genuine relationships and providing exceptional service that naturally encourages clients, friends, and family to recommend you. A well-structured system for nurturing these relationships can become a cornerstone of your marketing strategy, consistently generating valuable real estate leads.

Strategies for Encouraging Referrals:

Exceptional Client Service: The most powerful driver of referrals is providing outstanding service that exceeds client expectations. When clients are truly satisfied with their experience, they are naturally more inclined to recommend you to others. Focus on clear communication, proactive problem-solving, and going the extra mile.

Stay Top-of-Mind: Regularly connect with past clients through various touchpoints:

Personalized Check-ins: Send personalized emails, phone calls, or handwritten notes on anniversaries, birthdays, or other relevant occasions.

Valuable Content: Share helpful content such as market updates, home maintenance tips, or local community guides. This keeps you top-of-mind and positions you as a trusted resource.

Social Media Engagement: Engage with past clients on social media by liking, commenting, and sharing their posts. This helps maintain a connection without being overly intrusive.

Client Appreciation Events: Host client appreciation events, such as holiday gatherings, open house previews, or community events. These events provide opportunities to connect with past clients in a relaxed setting and strengthen relationships. These events must be free to attend and not contingent on referrals.

Request Feedback and Testimonials: Actively solicit feedback from clients after a transaction. Positive feedback can be used as testimonials on your website and marketing materials, further building your credibility and attracting new clients. This can also open the door for a conversation about referrals.

Express Gratitude: Always express sincere gratitude to anyone who refers you, whether with a handwritten thank-you note, a small gift (of nominal value and not contingent on a closed transaction), or simply a heartfelt verbal acknowledgment.

Increasing Visibility Through Community Involvement

Being active in the community shows you care and helps you generate real estate leads through trust and visibility. By volunteering, sponsoring local teams, or joining community groups, you meet people who value personal connections.

Community Involvement Ideas

Sponsor a Local Sports Team: Get your name on jerseys and connect with families who may need a buyer’s agent or seller’s agent.

Volunteer at a Local Charity: Build relationships with local leaders, who often become key centers of influence.

Host a Neighborhood Workshop: Teach residents about market trends, home values, and smart buying or selling strategies.

Example: One agent volunteered at a local food drive. While sorting donations, they met a range of people—small business owners, teachers, and young professionals—several of whom later approached the agent for help with property listings and to understand the current market trends.

Staying Connected With Past Clients

Past clients are a treasure trove of real estate referrals. By keeping these relationships warm, you remain top-of-mind when they—or their friends and family—need to buy or sell.

Follow-Up Methods

Personal Emails or Calls: Check in on their home’s value, update them on market trends, or see if they need any contractor referrals.

Handwritten Notes: Send a thank-you card or congratulate them on a home anniversary. A personal touch makes you memorable.

Social Media Engagement: Comment on their posts, share helpful articles on property listings, and offer tips about maintaining or increasing home values.

Example: An agent who helped first-time homebuyers regularly emailed them a yearly “Home Health Check” update, adding a personal touch to each message. This update included recent home values and market trends for their neighborhood. As a result, several past clients felt the warmth of the agent's communication and contacted them when family members started looking for homes, thus generating real estate leads without extra advertising.

At the heart of real estate lies the power of human connection. As a real estate professional, you'll create a thriving ecosystem of leads by prioritizing genuine networking, building trust with centers of influence, cultivating a strong referral network, actively participating in your community, and nurturing relationships with past clients. These personal connections not only open doors to unique property listings and enable you to serve buyers and sellers effectively but also establish you as a trusted and valued community member, deeply attuned to local market trends and home values.

So, what are your top strategies for attracting and retaining real estate clients through networking and referrals? Don't be shy, share your tips in the comments below!

Love,

Kartik

|

In today’s competitive real estate market, merely getting your real estate license and hoping clients come knocking on your door is not enough. Buyers and sellers alike have access to countless online Read more...

In today’s competitive real estate market, merely getting your real estate license and hoping clients come knocking on your door is not enough. Buyers and sellers alike have access to countless online resources, and they often seek social proof before entrusting a professional with one of the most significant financial transactions of their lives. This is where client testimonials come into play. By strategically gathering and showcasing authentic praise from past clients, you can boost your credibility, attract new business, and ultimately grow your real estate practice.

Below, I’ll explore why testimonials are so powerful, how to obtain high-quality endorsements, where to place them for maximum impact, and how to integrate them into your broader marketing strategy. You’ll also see example wording to inspire your testimonial requests and learn strategies for professionally addressing negative feedback.

Why Testimonials Are Powerful

Social Proof and Trust-Building: Testimonials are not just about showcasing your past successes, they are about building trust. They harness the power of social proof, a psychological phenomenon where individuals look to others to determine appropriate behavior or decisions. When a potential client reads about someone else’s positive experience with you, it signals that you are a trustworthy and capable professional. Testimonials help build a sense of reliability—qualities essential in a field where clients entrust agents with monumental personal and financial decisions.

Humanizing Your Brand: Real estate clients want to know that the person guiding them understands their needs. Testimonials are not just about showcasing your skills, they are about creating a personal connection. You transform yourself from a faceless salesperson into a relatable guide by sharing testimonials highlighting your market knowledge gained in the field and from your real estate license school. This comfort level can give buyers and sellers the confidence to engage with you before a face-to-face meeting.

Gathering High-Quality Testimonials

Timing Is Key: The best time to ask for a testimonial is shortly after closing when your client feels appreciative and excited about their experience. This ensures their feedback is authentic, vivid, and positive, enhancing the credibility of your business.

Method of Request: Consider a variety of methods to gather testimonials:

Email: A follow-up “thank you” email after closing is a natural time to request a brief written testimonial.

Video: A short video testimonial can be incredibly impactful if the client is enthusiastic and comfortable on camera.

Online Forms: Create a simple form with questions to guide clients through sharing their experiences. This straightforward process will make your clients feel at ease and comfortable with sharing their thoughts.

Questions to Ask (with Example Answers):

What concerns did you have before working with me, and how did I address them?”

Example Client Response: “Before meeting [Agent’s Name], we were worried about navigating the inspection process. Thanks to their knowledge (undoubtedly sharpened by bypassing the real estate exam) and clear explanations, we felt prepared and confident every step of the way.”

“How did I help make the buying or selling process smoother or more enjoyable for you?”

Example Client Response: “[Agent’s Name] took all the stress out of selling our home. They handled everything efficiently and kept us informed every step of the way.”

“Would you recommend my services to friends and family, and if so, why?”

Example Client Response:“We’ve already told several friends about [Agent’s Name]. Their professionalism, warmth, and knowledge made the experience exceptional.”

By asking open-ended, targeted questions and showcasing potential answers, you encourage clients to move beyond generic praise. This allows you to feature testimonials that highlight your unique strengths, such as your comprehensive real estate license education, market expertise, and negotiation skills, resonating with future leads and emphasizing your value.

Where to Display Testimonials

Your Website:

Your website is often the first place potential clients will look. Create a dedicated “Testimonials” or “Client Reviews” page featuring a mix of written quotes and short video clips. To make this page more engaging, consider adding photos of the clients or the properties they purchased. Highlighting names, neighborhood locations, and property types helps potential clients relate more easily. Include featured testimonials throughout the site—on your homepage, services page, and contact page—to reinforce credibility at every stage of the visitor’s journey.

Social Media Platforms:

Utilize the power of social media platforms like Facebook, Instagram, and LinkedIn to showcase short, visually appealing testimonial graphics or brief video clips. The casual nature of these platforms allows testimonials to feel organic and personal, thereby strengthening trust and making a significant impact on your marketing strategy.

Marketing Materials:

Printed brochures, flyers, and listing presentations are powerful tools in your marketing arsenal. Incorporating snippets of testimonials into these materials can provide a sense of reassurance to prospective clients, helping you stand out from competitors and build trust.

Online Review Sites:

Encourage clients to leave reviews on reputable third-party review sites like Google My Business, Yelp, or Zillow. These platforms add an extra layer of credibility to your business. Potential clients who find you through these portals will be exposed to positive feedback before even reaching your website, enhancing your reputation.

Types of Testimonials and How to Use Them

Written Testimonials:

Written endorsements are incredibly versatile and easy to display. To spark interest, use concise excerpts—one or two sentences—on social media and marketing collateral. For those who want to delve deeper, reserve longer, more detailed testimonials for your website, where potential clients can invest time reading them in-depth. This flexibility allows you to cater to different audience preferences.

Video Testimonials:

Video Testimonials: Video testimonials bring a dynamic, human element to your marketing. The visual and auditory experience of seeing and hearing a client speak positively about your services can have a profound effect, surpassing the impact of text alone. Include these videos on your website’s testimonial page and share short clips on social media. High-quality video testimonials can also be included in listing presentations, allowing prospective clients to witness genuine satisfaction.

Audio Testimonials:

Though less common, audio testimonials (e.g., short recordings or podcast snippets) can be surprisingly impactful, especially if you already produce audio or video content. They add variety and help you stand out in a crowded marketplace, showing the potential of this form of endorsement.

Addressing Potential Concerns

Ethical Considerations:

When sharing testimonials, always prioritize truth and accuracy. Avoid any form of misrepresentation by refraining from editing client’s words. It's also advisable to seek written permission before using their testimonials publicly, as this demonstrates your commitment to ethical practices.

Handling Negative Feedback:

When faced with negative or lukewarm reviews, view it as an opportunity to showcase your professionalism and dedication to customer service. Instead of ignoring or dismissing the feedback, consider the following approach:

When responding to feedback, always do so with a calm and empathetic tone. Acknowledge the client's experience and express regret that it didn’t meet their expectations. This approach shows respect for the client's experience and can help defuse a potentially negative situation.

Take It Offline: Suggest discussing the matter privately to gain insight and possibly rectify the situation. “I’d love the opportunity to understand what went wrong and make it right. Please get in touch with me at [phone number] or [email address].”

Commit to Improvement: Emphasize the value of continuous learning and improvement in your professional journey. Use the feedback to enhance your skills and later, you can proudly mention how your additional training and courses through real estate license school enable you to serve future clients better.

Lack of Testimonials:

If you’re new to the industry, consider asking past employers or colleagues for character references that speak to your work ethic and integrity. As you build your clientele, you will gain testimonials from buyers and sellers that reflect your unique strengths.

Integrating Testimonials into Your Marketing Strategy

Email Campaigns:

Include brief testimonial snippets in your email newsletters or drip campaigns. These testimonials, when sent as a follow-up message after an open house, add a short quote from a satisfied buyer. This subtly reinforces your credibility and real estate expertise, reassuring your audience of your capabilities.

Social Media Posts:

Regularly share new testimonials on your social media channels. It's crucial that these testimonials are authentic and reflect real experiences. Pair them with a friendly headshot of the client (with their permission) or a picture of the property they purchased or sold. These personal details, when authentic, build trust and remind your audience that others have had great experiences with you.

Advertising:

Consider using testimonials in your paid advertising, both online and in print. A well-placed testimonial in a targeted Facebook ad campaign can make your message more compelling and credible, convincing your audience of your value.

Client testimonials are powerful tools that can significantly enhance your credibility and attract new business. By skillfully asking for feedback, choosing the right platforms for display, and integrating testimonials into your overall marketing plan, you’ll not only leverage the trust and social proof needed to stand out, but also attract new business. Whether you’re just earning your real estate license or have been practicing for years, these methods help ensure that your hard-won expertise—honed through real estate license school and validated by success on the real estate exam—translates into continued growth and a thriving career.

Love,

Kartik

|

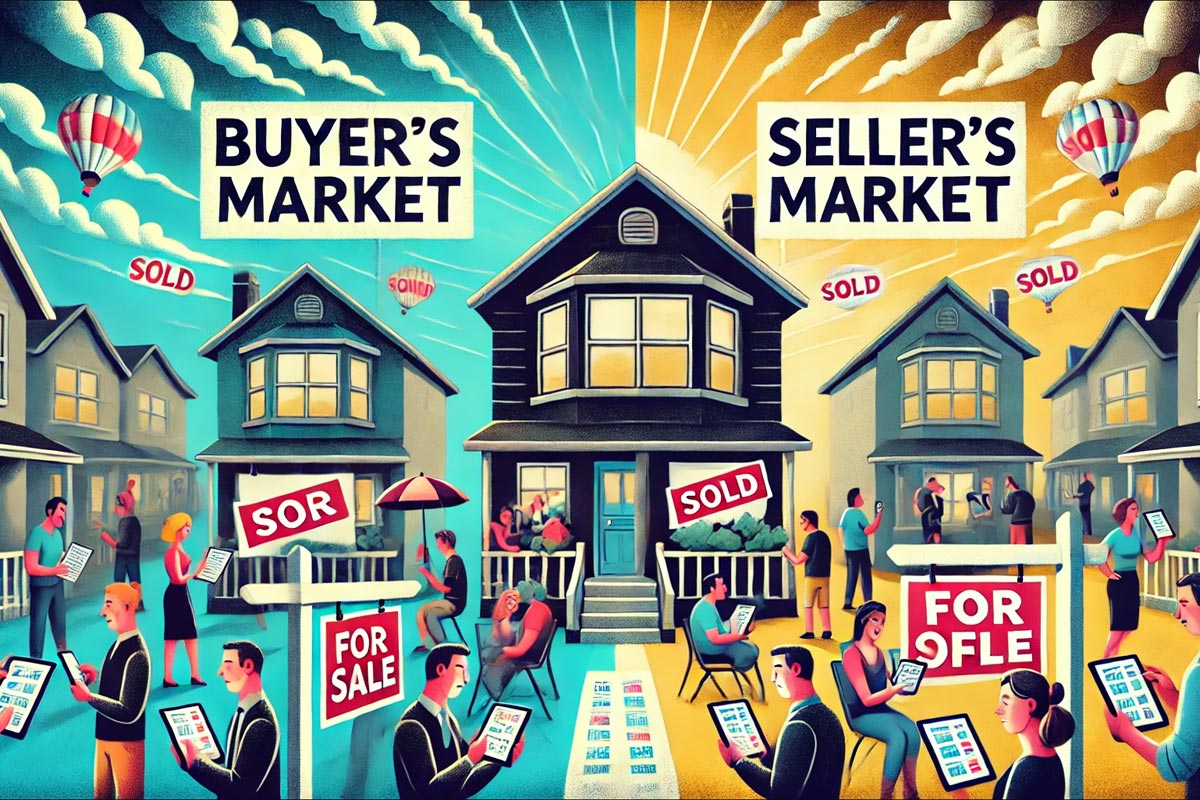

Why Understanding Market Indicators Matters

Want to excel as a real estate agent? Mastering market analysis is essential, and it's a skill you can start developing now, even while you're still Read more...

Why Understanding Market Indicators Matters

Want to excel as a real estate agent? Mastering market analysis is essential, and it's a skill you can start developing now, even while you're still in real estate school. Understanding market trends empowers you to advise clients effectively, price properties accurately, and anticipate market shifts. This guide breaks down the key indicators—median and average home prices, days on market (DOM), inventory levels, interest rates, foreclosure rates, and the absorption rate—providing clear explanations and practical examples. I’ll show you why a holistic approach to market analysis is crucial and how local conditions and seasonality influence these metrics. By the end, you'll have the knowledge and confidence to navigate any market.

Median vs. Average Home Price

Median Home Price:

The median home price is the middle price of all homes sold in a particular area during a given time.

For example, if five homes sold for:

$200,000

$220,000

$250,000

$600,000

$700,000

The median is $250,000 (the one in the middle).

The median, being less affected by outliers, is a reliable measure when there are a few very expensive or very cheap homes that could make the average less accurate.

Average Home Price:

To find the average home price, you simply add up all the sold home prices and divide by the number of homes. Using the same prices above, the total is $1,970,000. Divide that by five, and you get an average of $394,000.The average, while useful for spotting general trends, can be heavily skewed by extremely high or low prices, making it less reliable in such cases.

What These Prices Tell Us:

If median and average prices are rising, it often means home values are going up. If they’re falling, it might mean the market is slowing down.

Days on Market (DOM)

Days on Market (DOM) measures how long a home takes to sell.

Short DOM (under 30 days): Suggests a hot market with many interested buyers. This is often called a seller’s market because sellers have the upper hand.

Medium DOM (30-60 days): A balanced market where buyers and sellers have similar power.

Long DOM (60+ days): Suggests a more extraordinary market with fewer buyers. This is often called a buyer’s market because buyers have more choices and bargaining power.

Inventory Levels (Months’ Supply of Inventory)

Ever wondered how long it would take to sell all the homes on the market if no new ones were listed? That's what a month's supply of inventory tells us.

How to Calculate:

Months’ Supply = (Number of Homes for Sale) ÷ (Number of Homes Sold per Month)For instance, if there are 600 homes for sale and 200 sell each month, you can easily calculate the months’ supply as 600 ÷ 200 = 3 months, giving you a clear picture of the market conditions.

Low Inventory (Under 4 Months): Seller’s market.

4-6 Months: Balanced market.

Over 6 Months: Buyer’s market.

Interest Rates

Interest rates affect how much it costs to borrow money to buy a home.

Low Interest Rates: More people can afford homes, so demand usually goes up.

High Interest Rates: Fewer people can afford homes, so demand usually slows down.

The Federal Reserve’s policies can influence these rates, so it’s smart to keep an eye on their announcements.

Foreclosure Rates

Foreclosure rates tell us how many homes are being taken back by lenders because their owners cannot pay their loans.

If foreclosures are high, it can mean that the economy is struggling, and home prices might drop because many distressed properties hit the market.

Foreclosure data can be found on local government websites, local MLS systems, or online real estate data providers.

Absorption Rate

The absorption rate shows how fast homes are selling in a certain area.

How to Calculate: Absorption Rate (%) = (Number of Homes Sold in a Given Period ÷ Number of Homes Available) × 100

For example, if 100 homes are for sale and 20 sell in one month, the absorption rate is (20 ÷ 100) × 100 = 20%.

A higher absorption rate means homes sell quickly (seller’s market), while a lower rate means they sell slowly (buyer’s market).

Seasonality: How the Time of Year Affects Indicators

Real estate activity often changes with the seasons.

Spring and Summer:

These seasons are a hotbed for real estate activity. Many buyers are on the lookout for homes when the weather is pleasant and before the new school year begins. This surge in demand often results in shorter DOM and escalating prices.

Fall and Winter: These seasons bring a shift in real estate dynamics. With fewer buyers in the market due to colder weather and holiday distractions, homes may take longer to sell. Prices, in turn, tend to remain stable or experience a slight dip.Understanding how seasonality affects your local market is not just a skill, it's a responsibility. It can help you advise clients on the best time to list or buy a home, ensuring they make the most informed decisions.

Looking at Indicators Together: Two Scenarios

Relying on one number can be misleading. By using multiple indicators, you get a clearer picture.

Scenario 1: Seller’s Market

Median Home Price: Rising for the last six months.

DOM: Dropped from 40 days to 15 days.

Inventory: Went from 5 months to 2 months of supply.

Interest Rates: Remain low.

Foreclosures: Very few.

Absorption Rate: Increased to 25%.

Analysis: Everything points to a seller’s market. Prices are going up, homes sell fast, inventory is low, rates are low, and there aren’t many distressed sales. This means sellers can expect strong offers and may not need to lower their asking prices.

Scenario 2: Buyer’s Market

Median Home Price: Flat or slightly decreasing.

DOM: Increased from 30 days to 60 days.

Inventory: Rose from 4 months to 7 months of supply.

Interest Rates: Slightly higher than last year.

Foreclosures: A bit higher than normal.

Absorption Rate: Dropped to 10%.

Analysis: In this market, buyers have more choices, and homes sit on the market longer. With rising inventory and slower sales, buyers can negotiate more and might get lower prices or better terms.

How Market Indicators Affect Appraisals

Appraisers look at recent home sales and market trends to determine a home’s value. It's crucial to understand that market conditions can significantly influence appraisal values. In a hot seller’s market with rising prices and low inventory, an appraisal might come in higher because comparable homes sell quickly and at higher prices. In a slower buyer’s market, appraisals might reflect lower prices, especially if there are many homes for sale and fewer sales to compare against.

Focusing on Local Data: More Specific Sources

Real estate is local. National numbers can give you a big-picture idea, but local data tells you what’s really happening in your area. Here are a few resources to help you find local information:

Local MLS Systems: For example, CRMLS in California or Stellar MLS in Florida provide data on listings, sales, and DOM.

Government Websites: The U.S. Census Bureau can provide population and housing data. Some cities and counties also have their own websites with housing reports, like NYC Housing and Vacancy Survey.

Real Estate Portals: Websites like Realtor.com Local Market Trends or Zillow Research can offer local statistics on prices, rent, and more.

By checking these sources, you can get the most accurate information for the neighborhoods where you work.

The Limits of Market Analysis

Market indicators can help you understand what’s happening, but they aren’t crystal balls. Conditions can change quickly due to new jobs in town, changes in mortgage rules, or shifts in the local economy. Also, predictions based on indicators are not guaranteed. It's crucial to be cautious and mindful, remembering that these tools guide your decision-making but don’t always tell you exactly what will happen in the future.

Putting Your Knowledge into Action

By learning about these market indicators, you can better guide your clients, set fair prices, and know when to act. Remember to look at multiple indicators at once to get the full story. Also, focus on local and seasonal trends, pay attention to how conditions affect appraisals, and understand that no analysis is perfect.

If you want to dig deeper, we encourage you to take action:

Enroll in our real estate licensing course to gain more in-depth market analysis skills.

Contact us for a free consultation to discuss your real estate career goals.

By staying informed, you can make smarter decisions and stand out as a trusted real estate professional.

Love,

Kartik

|

What Are HOA Fees?

Homeowners Association fees are regular payments made by every property owner in a condominium or townhome community. They help cover shared expenses like maintenance, insurance, Read more...

What Are HOA Fees?

Homeowners Association fees are regular payments made by every property owner in a condominium or townhome community. They help cover shared expenses like maintenance, insurance, and the amenities you enjoy, ensuring everyone contributes their fair share. This shared responsibility keeps the property’s appearance, safety, and value consistent, benefiting all residents.

What Do HOA Fees Cover?

Most HOA fees focus on four main areas: maintenance, insurance, amenities, and reserve funds. Let’s break each one down further.

Maintenance

Landscaping: Caring for lawns, bushes, trees, and flowers to keep the community looking fresh and inviting.

Snow Removal: Clearing driveways, walkways, and parking areas during the winter to keep residents safe.

Common Area Cleaning and Repairs: Maintaining hallways, elevators, lobbies, and other shared spaces so everyone enjoys a clean, well-kept environment.

Insurance

A master insurance policy protects the building and common areas against fires, storms, or vandalism damage. While individual homeowners still need personal property insurance (often called an HO-6 policy) to cover belongings and the interior of their units, the HOA’s insurance takes care of the larger structure and shared grounds.

Amenities

Amenities vary, but your HOA fees might cover:

Pool Maintenance: Keeping the pool clean, safe, and ready for use.

Gym Maintenance: Ensuring exercise equipment is well-maintained for convenient, on-site workouts.

Clubhouse Maintenance: Preserving shared gathering spaces for parties, meetings, or community events.

These perks can increase your quality of life and enhance your property’s resale value.

Reserve Funds

A portion of your monthly fee goes into a reserve fund, which acts like a community savings account. It’s used for capital improvements and major repairs, such as replacing the roof or repaving the parking lot. By saving over time, the HOA can handle these larger projects without surprising you with big, last-minute bills, providing financial stability and peace of mind.

How Are HOA Fees Calculated?

Your HOA board creates an operating budget each year. They often conduct a reserve study to predict future maintenance and repair needs, providing a sense of security and preparedness. The HOA ensures fair contributions by estimating the total annual costs and dividing them among all units.

As a homeowner, you have the right to access the HOA’s budget documents and reserve studies, often through the HOA management company’s website or an online portal. This transparency empowers you to understand how your fees are used and ensures community accountability.

High vs. Low HOA Fees: What’s the Difference?

While lower fees might initially seem appealing, it's important to consider the long-term implications. They can sometimes lead to limited maintenance, fewer amenities, and smaller reserve funds. Over time, this can cause deferred maintenance, which may lower your home’s resale value. By being aware of these potential outcomes, you can make an informed decision about your investment.

For instance, let's consider a community in Rancho Cucamonga with low HOA fees of $ 100 per month and a community in Newport Beach with high HOA fees of $ 500 per month.

Scenario A (Low HOA Fees): The fees are low, so the community provides only basic landscaping and minimal exterior upkeep. Amenities are scarce, and repairs are postponed due to limited funds. Over the years, the property’s appearance has suffered, which may reduce its overall value.

Scenario B (High HOA Fees): The fees are higher, enabling the community to maintain beautifully landscaped grounds, conduct regular exterior building maintenance, and offer luxurious amenities such as a resort-style pool and a state-of-the-art fitness center. With well-funded reserves, the HOA can handle significant repairs without issuing special assessments. This ensures that the property remains attractive and can even increase in value over time, providing a sense of security for your investment.When choosing a community, it's crucial to consider what you get in return for the fees. Sometimes, paying more each month means fewer surprises and a more enjoyable living experience. By understanding the role of HOA fees in shaping your living experience, you can make a decision that aligns with your lifestyle and preferences.

Understanding Special Assessments

While the regular budget and reserve funds are crucial, they may not always cover unexpected issues like severe storm damage or sudden major repairs. In such cases, the HOA might issue a special assessment, a one-time fee in addition to your regular dues. This can be seen as a proactive measure to protect your investment and ensure the community's well-being.

Before buying, ask about the community’s history of special assessments.

It’s important to find out how often they’ve occurred and why they were needed. Understanding this can give you insight into how well the HOA plans for the future and handles emergencies.

Why HOA Fees Matter

Property values, community upkeep, curb appeal, and resale value all benefit from a well-funded and well-managed HOA. By paying HOA fees, you actively contribute to keeping common areas attractive, ensuring repairs are done on time, and maintaining amenities that enhance your quality of life and your home’s value. Your fees are not just a financial obligation, but a direct investment in your community's improvement.

These fees aren’t just another bill but an investment in your community’s future. With substantial financial planning, the HOA can keep your property looking great, making it a place you’re proud to call home. By understanding and being part of this planning, you can feel more empowered and informed about your community's future.

HOA fees (condo fees or HOA dues) are essential to condo or townhome ownership, and your role in understanding them is crucial. They pay for upkeep, insurance, amenities, and future repairs that keep your property safe, comfortable, and visually appealing. By taking time to understand the HOA’s budget, reserve funds, and history of special assessments, you can make a well-informed decision, knowing that your input is valuable.

If you’re still exploring your housing options, remember there’s a difference between condos and apartments. Equipped with this knowledge, you can feel confident you’re making the right choice for your lifestyle, budget, and long-term investment.

Love,

Kartik

|